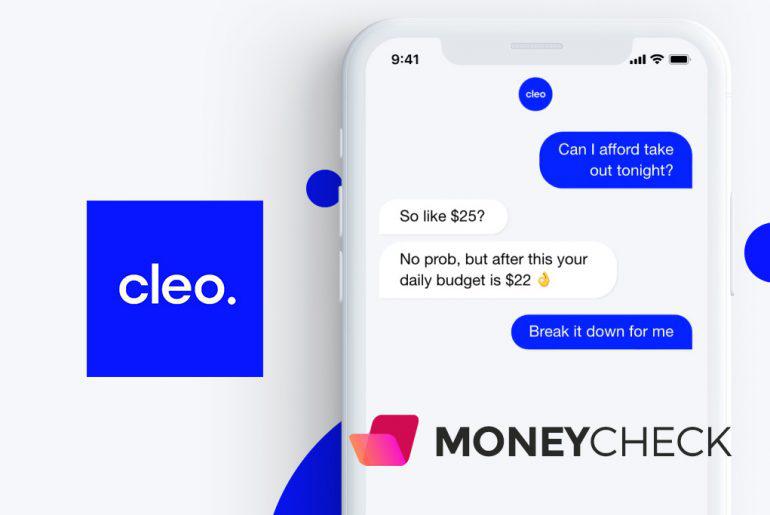

Ever woken up with last night’s makeup still on, an uneaten slice of pizza on the bedside table, a jackhammer in your head, and an account balance that only adds to your already rising nausea? Ever spend way too much on take-out because you’re just too exhausted from your job—that doesn’t pay you nearly enough